Every so often, I write about this cheery subject but it really is worth getting to know the basics if you do not want to suffer from, or leave your beneficiaries exposed to, the slings and arrows of outrageous tax complications. There are proposed changes to UK inheritance tax which I will discuss below.

Viewing posts from: November 2000

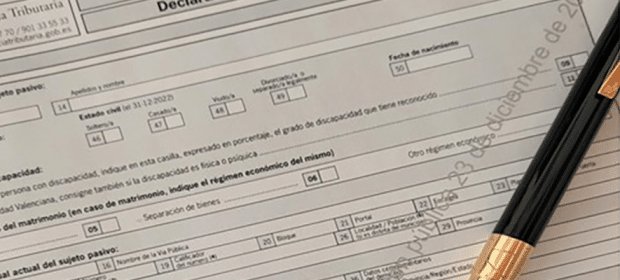

UK Inheritance tax and living in Valencia

By John Hayward

This article is published on: 30th April 2024

30.04.24

Inheritance tax in Spain has pretty much disappeared, for some and for the time being. For example, in the Valencian Community, there is an inheritance tax (and gift tax) allowance of €100,000 for spouses, grandparents, parents, children, and grandchildren. For younger beneficiaries, the allowance is higher, as it is for those with qualifying disabilities. Since 28th May 2023, there is also a 99% reduction on the tax bill for spouses, etc. This means that there is little or no tax due for the relevant category. I am not going to write about the different tax bandings but you can contact me if you want to know more.

Taxes in Spain tend not be abolished but rather put on hold or reduced, temporarily. In Valencia, this “new” 99% reduction is the same as the old 99% reduction which was in place up until 2013 when it was reduced to 75% and subsequently 50%. Asset distribution is an important consideration, making certain that, should the thinkable happen, i.e. the reduction is changed again, spreading wealth as tax efficiently as possible is key. (Spending everything is also a way of reducing any inheritance tax liability albeit to the disappointment of those expecting some handy cash.)

When it comes to beneficiaries who do not tick the right boxes, planning is even more important. One of the fairly common situations I have come across is where couples in their second or third marriage have children, from different marriages, who are beneficiaries on the death of their parent and/or step-parent. The inheritance tax allowances above do not apply if the child is not a direct relative.

Allocating assets through a will could alleviate this problem. Spain will apply inheritance tax to an asset in Spain or an individual resident in Spain. A UK asset inherited by a UK resident will not be subject to Spanish tax.

Therefore, planning is necessary to decide which child receives which asset. (See below for proposed UK inheritance tax change).

Although you might read that the double taxation agreement between Spain and the UK does not cover inheritance tax, tax paid on the UK estate can be deducted proportionately from the individual’s tax liability in Spain.

Proposed changes to UK inheritance tax

The UK government is looking to move from a domicile basis to a residence basis. To determine where one is domiciled can be a complicated exercise.

The UK government website states: HMRC will treat you as being domiciled in the UK if you either:

- lived in the UK for 15 of the last 20 years

- had your permanent home in the UK at any time in the last 3 years of your life

The proposed change, effective from 6th April 2025, will be to charge individuals who have been UK resident for 10 years and keep them on the radar for 10 years after leaving the UK. This would mean that after 10 years in, say, Spain, only UK assets would be subject to UK inheritance tax. This leads us back to my point about asset distribution. Where possible and necessary, assets should be allocated to beneficiaries based on their residence to maximise the tax allowances in both the UK and Spain.

We specialise in arranging savings and investments in a tax efficient manner and have saved clients and their families thousands in taxes on the death of a spouse, partner, or parent, or even an unknown uncle in one case. I am certain that we can help you too.

Interest in deposit accounts

By John Hayward

This article is published on: 11th January 2024

11.01.24

Timing when to invest for long term needs is trickier than solving a Rubik’s Cube wearing boxing gloves

As we enter a new year, we face another year of known and, so far, unknown global problems which could impact our finances. Many “experts” will guess and then advise us what will happen but, as so often in the past, be wrong, or lucky if the guess works out to be true. The world is governed by a handful of people. Therefore, there are very few who really know what is happening.

Fortunately, in the Western world at least, we are allowed to get on with our lives with an element of freedom. As financial advisers, especially as old as me, we can make some judgement based on how people react to global events. Some people over react, fed by questionable journalism. In the investment world, this leads to the wealthy becoming wealthier aided by panic selling by the less wealthy enabling the wealthier to buy into the market at a lower cost.

2022 was a rotten year overall for investments. 2020 was not great but people then were more concerned about living with Covid-19 than what was going on with their money. Stock and bond markets both had a torrid time, mainly as a consequence of Covid-19 which introduced high inflation once we had a chance to spend money again. A consequence of this was a reluctance in 2023 to commit to investing at a time where inflation was rampant. History has shown us that investing in traditional markets can overcome inflation. With high inflation came attractive interest on cash, something that we had not seen in decades. Back to the history book and we see that interest rates on deposit accounts have not outpaced inflation over the long term. However, the expression “long-term” seems to disappear from the vocabulary of some investors and short-term problems become the index to follow. Many have caught the interest rate bug over the last few months feeling that doing this would be sensible in the short term and then switch into investment markets when the time is right(?). Paraphrasing Jim Bowen of Bullseye fame, “Let’s look at what they could have won” had they not taken this approach.

Let us look at two different examples of investors. One who was invested on 1st January 2022 with 50% in the Rathbone Strategic Growth fund and 50% in Aegon High Yield Bond fund who decided to sell on 31st December 2022 due to the downturn in 2022 and another who was thinking about investing on 1st January 2023 but decided not to. In both cases, they eventually put their cash into a deposit account with a fixed rate of 5% (for 12 months) in July 2023.

| 1/1/22 to 31/12/222 | 1/1/23 to 31/12/23 | |

| Rathbone and Aegon | -9.10% | 11.45% |

The person who sold from the two funds at the end of 2022 was 9.10% down for the year and only recouped 2.50% (6 months at 5% p.a.) by the end of 2023 instead of 11.45%.

In a similar way, the potential investor, who was holding off until things improved, missed that particular bus. Again 2.50% versus 11.45%. I appreciate that there are underlying charges with our products but nowhere near 9% a year and there are also tax considerations with the deposit account being taxed annually whereas the Spanish compliant bonds that we promote have tax deferred, if not completely negated.

Very few are smart enough or knowledgeable enough or lucky enough to time markets correctly. In the last year we have seen this proven once again.

When I tell people that they should be prepared to leave their money invested for at least 5 years, I often get the response that they are not young and that they may not survive 5 years. In a region such as the Costa Blanca where I live, with 300 plus days of sunshine a year and plenty of olive oil, the risk people face is living too long! In the “good old days” when the life expectancy was 65 or less, long term care and dementia were not a consideration. Making money work over the long term is not only a good idea but possibly essential.

We have products that can work with you and your family throughout your life, and beyond. Following the scaremongering headlines is not a great idea and can be very harmful to your wealth, and your health.

I know that it is possible to solve a Rubik’s Cube wearing boxing gloves but try it.

Reduction of Succession and Gift Tax in Valencia

By John Hayward

This article is published on: 29th November 2023

29.11.23

Making gifts to spouses is no longer a tax worry.

In September, the Valencian government approved the draft bill reducing succession tax (Inheritance tax) and gift tax for certain beneficiaries

The reasons were that the taxes formed a very small part of the region’s revenue and many people were refusing inheritances as the tax worked out to be more than the overall benefit. Does the son or daughter in the UK really want to inherit the casita in the campo housing pigs and chickens?

We have had to wait for the bill to become law and this occurred on 24th November 2023 taking effect from 28th May 2023, the date that Carlos Mazón was elected president of the regional government of Valencia as leader of the Partido Popular. The backdating of this law is significant for beneficiaries who are dealing with deaths and inheritances since 28th May.

It is important to understand that the taxes for certain beneficiaries have been reduced but not abolished. The reduction in the tax has increased from 50% to 99% of the tax bill. This reduction applies to Class 1 and Class 2 beneficiaries and includes the proceeds of life insurance. These classes cover children, grandchildren, adoptees, parents, grandparents, adopters, and spouses. The €100,000 allowance per qualifying individual beneficiary (up to €156,000 for children under 21) will remain.

Suggesting that it is a better time to die now may sound a little crass but it would appear to be a very good time to make gifts, taking advantage of the gift tax reduction and mitigate future succession tax. Another important aspect to gifts is that they need to be formally documented.

Over the last 10 years, Valencia has changed the basis of succession and gift tax on a number of occasions. There was a 99% reduction before. This fell to 75%, then 50%, and is now back up to 99%. Therefore, it is reasonable to suggest that there could be changes to the law again.

Strangely, before these revisions, spouses in the Valencian Community did not receive an allowance on gifts and this caused a problem when planning financial structures. Spouses in the Valencian Community are now eligible for the allowance of €100,000 on gifts along with the 99% reduction on the tax on any excess. In my case, the “What’s hers is hers and what’s mine is hers” principle still applies.

Contact me to discuss ways of reducing the tax liability for those you care about no matter what the law is at the time.

The end of succession tax in Valencia

By John Hayward

This article is published on: 6th September 2023

06.09.23

On 28th May 2023, Carlos Mazón was elected president of the regional government of Valencia as leader of the Partido Popular. On 21st July 2023 he announced that his government had approved the initiation of a bill to reduce succession and gift tax (ISD – Impuesto de sucesiones y donaciones – Inheritance Tax to the UK reader).

The draft bill was placed on the urgent pile with Les Corts on 3rd August 2023 and it awaits absolute approval.

Mazón’s reasoning was that the income from ISD represents around 1% of the region’s total revenue and that charging tax on money that has been taxed before was not fair. He wants to reduce the tax burden to prevent an inheritance from becoming a “serious economic loss for many families, who have to face its payment, without the inheritance entailing any economic benefit or real increase in their assets.” This seems a very refreshing attitude although his opposition have argued that the wealthy will avoid tax that would generate around €400 million a year. This assumes that the timing of deaths and gifts matches their statistics.

There are conditions to this bonificación in that only close family members and spouses will benefit but that is the same with the existing reduction. The improvement is that, for the majority of spouses and close family members, they will receive a reduction of 99% on the tax bill. Currently it is only 50%.

All this being said, there is still room for inheritance tax, and gift tax, planning. We experience many complicated situations where, for example, couples are not married or there are children from different marriages. Keeping assets away from the inheritance and gift tax net in Spain, in a legal way, is key, especially for beneficiaries who do not live in Spain.

We await absolute approval of the bill but, and although this may sound a little insensitive, any deaths, and gifts made, since 28th May 2023 will be eligible for this new law.

And like buses… Abolition of Wealth Tax in Valencia?

One at a time, please!

More to follow…

To find out how Spanish inheritance and gift tax will affect you and your beneficiaries, as well how we can help you with your existing investments and tax planning, and provide you with ideas for the future, contact me today at john.hayward@spectrum-ifa.com or on +34 618 204 731 (WhatsApp)

Reducing Spanish tax

By John Hayward

This article is published on: 27th June 2023

27.06.23

Use a beneficial savings structure

Investing money is often seen as a risky thing to do even though it is generally understood to be necessary. For example, those receiving pension income would not be in the same position if the companies paying the income had left all of the pension contributions in a current account or in a box under the bed.

Financial markets can be volatile (always, I hear you shout). We fully appreciate this. We also acknowledge that inflation has created higher interest rates. Better news if you are a saver but not so pleasant for mortgage payers, or parents having to help their children pay off increased debt.

Let us imagine that, for the foreseeable future, we have high inflation accompanied by higher interest rates. Using an amount of £500,000, I have compared depositing in a savings account with investing in a Spanish compliant investment bond and I have used an interest/growth rate of 4%. I have based my comparison on the bond paying growth to the bondholder’s bank account and using GBP as I cannot see any Euro accounts paying 4%.

– £500,000 at 4% = £20,000

– Using an exchange rate of 1.16 £/€,

– £20,000 = €23,200

The deposit account interest is taxed in full and, at current 2023 rates, is €4,752 each year. This has to be declared in the annual tax return.

The Spanish compliant bond attracts tax on the gain within the withdrawal. I have based the calculation on the same amount being withdrawn i.e., €23,200. In the first year, the taxable gain within this is only €892 and the corresponding tax is €170. The taxable amount within the bond income increases over time but, over 10 years, the tax is:

– €47,520* on the deposit account interest

– €8,381* on the bond income

This gives a tax saving of over €39,000 over 10 years by using the Spanish compliant bond.

If no money is withdrawn from the bond, no tax is payable whereas the interest on the deposit account will continue to be taxed.

If the bondholder moved back to the UK, and nothing had been withdrawn whilst living in Spain, any growth on the bond whilst resident in Spain would be ignored by the UK tax office.

As an added benefit of reducing taxable income, wealth tax can be reduced. See this Wealth Tax in Spain article.

There can also be inheritance tax benefits with the bond when compared to the deposit account.

Well managed portfolios have consistently outstripped inflation. Conversely, deposit interest rates offered to savers have consistently under-performed inflation over the years.

To find out how we can help you with your existing investments and tax planning, and provide you with ideas for the future, contact me today at john.hayward@spectrum-ifa.com or on +34 618 204 731 (WhatsApp)

* E&OE. The above is a simplified example for illustrative purposes and general guidance only.

How to reduce Wealth Tax in Spain

By John Hayward

This article is published on: 21st June 2023

21.06.23

Earlier this year, I wrote an article about the introduction of solidarity tax in Spain. This is a “temporary” (we shall see) tax on wealth for those with more than €3,000,000 in assets. This is in addition to wealth tax although any wealth tax due can be deducted from the solidarity tax bill. (This is not the case for residents of the Madrid or Andalusia regions as there is no Wealth Tax currently).

I have been working with clients who are affected by these taxes, trying to find ways of reducing the tax liability. Reducing wealth by gifting to, say, children is an option but that can create additional immediate tax problems. Also, for a number of different reasons, some clients are not willing to gift anything in their lifetime.

The amount of wealth Tax that has to be paid can be governed by income. Your income tax and wealth tax cannot exceed 60% of your total taxable income.

Example:

– Total taxable income is €40,000

– Tax payable €8,000

– Assets subject to wealth tax €3,000,000

– Wealth tax due €39,000

– The maximum that can be paid when adding income tax and wealth tax together is 60% of the total taxable income (€40,000).

– €40,000 x 60% = €24,000

Therefore, the maximum wealth tax that can be paid is €16,000 (€24,000 less €8,000 income tax).

However, having to pay €16,000 a year in wealth tax is still not particularly nice. What we can do is look at the income in order to see if this can be restructured. Notable targets for this type of planning are savings interest (more relevant at the moment) and income/dividends from shares and investment funds. By careful planning, we can provide the same level of income yet reduce the tax. Please visit this Tax Benefits of a Bond page which illustrates one of the major benefits of a correctly structured investment bond which not only reduces income tax but also helps to reduce wealth tax.

To find out how we can help you with your existing investments, pensions, and tax planning, and provide you with ideas for the future, contact me today at john.hayward@spectrum-ifa.com or on +34 618 204 731 (WhatsApp)

History: How it can save you money

By John Hayward

This article is published on: 31st May 2023

31.05.23

“If you think you have it tough, read history books.” Bill Maher

I was not particularly interested in history at school, mainly because the history masters (I went to a grammar school where we were taught by masters in moth-eaten gowns and who wore their ties outside their jumpers) would want to teach us about aspects that I had absolutely no interest in.

The Dark Ages, for example. They are called dark ages for a reason. These days I will happily surf the web (can we still say that?) going off-piste (no holding me now) and finding out brilliant historical facts that I am interested in and not what I am told to be interested in. Or maybe I am being told, in this Artificial Intelligence world that we now live in. Having said that, I have not felt any pressure to learn any more about the dark ages.

What is my point here? History is important because it can help us to make decisions. The problem is that, although we have plenty of information to refer to, and perhaps have taken on board, we all too often forget, or even choose to ignore, the “lesson”. In the investment world, it appears that everything that is happening now never occurred before. Or maybe it did but in a dark age when nobody was literate enough to write down what was going on.

Sell low, buy high. Isn’t that a ridiculous investment strategy? It seems not, to some. I have been in the company of many people over the years who believe that they know when to sell and when to buy back in when “things are better/markets have settled/it is less rainy/the dog has been to the vet”. This strategy has consistently proven itself to be flawed. Although past performance is no guarantee of future performance, history can give us an idea of what could happen in the investment world after different global events. In more recent years, the financial crisis of 2008 and Covid-19 in 2020 have been big tests. After both “incidents”, those who stuck with it have been better off.

Source: Financial Express

Focusing on a stock market index that many British people are familiar with, the FTSE100, in the last 15 years to 1st May 2023, there have been 4 years that have been negative. I apologise for spelling this out but that means 11 years have been positive. 11-4. I like that score. The average annual gain of the index over that period has been almost 13%. Even more interesting is the tendency that a bad year is followed by an outstanding one. This is why, when people sell, they crystallise a loss and then possibly miss the best part of any recovery.

I understand that not everybody is comfortable with sitting out large falls (2008 and 2020). To cater for this, we have solutions within our armoury which limit the downside whilst still providing long-term growth.

To find out how we can help you with your existing investments, and/or provide you with ideas for the future, contact me today at john.hayward@spectrum-ifa.com or on +34 618 204 731 (WhatsApp)

If you are feeling down, pick up a history book. It is certain to take your mind off your woes.

Am I paying too much Wealth Tax in Spain?

By John Hayward

This article is published on: 21st February 2023

21.02.23

Just when you thought that it was safe to win the lottery in Andalusia or Madrid, the socialist Spanish government have introduced a new

temporary Solidarity Tax.

According to Investopedia, a solidarity tax is a government-imposed tax that is levied in an attempt to provide funding towards theoretically unifying (or solidifying) projects. In other words, it is a tax on the wealthy to provide funds for the not so wealthy. Other regions still have Wealth Tax with varying allowances and this will continue without the risk of having to pay two taxes. That said, taxes are rarely straightforward and I am confident that there will be issues in the future which will result in the Spanish tax office tweaking things. It is interesting, if not extremely concerning, that Wealth Tax was introduced on a temporary basis as well. It has been around for the last 11 years. So, not really temporary in my opinion.

We are in Modelo 720 season at the time of writing, with overseas assets having to be declared by 31st March. Although not a tax declaration, the Modelo 720 naturally leads on to Wealth Tax. One of the asset types to declare is property.

In Spain, the tax office can reference the Cadastre to establish a property value. However, they do not have access to the land registry in, say, the UK. Therefore, the only price that is in writing is the purchase price. It is this value that should be entered on the Modelo 720 and subsequently be liable, or not, for Wealth Tax. My suspicion is that people have declared what they believe to be the market value and are possibly paying too much in Wealth Tax as a consequence.

By redistributing wealth and utilising the allowances, and applying the 60% rule (contact me for more information), it is possible to reduce Wealth Tax (and/or Solidarity Tax) or even eliminate it completely.

We can introduce you to investment products that are not only tax efficient in Spain in terms of income tax but can help to reduce Wealth Tax.

More Spanish residents to pay wealth tax

By John Hayward

This article is published on: 19th January 2023

19.01.23

Valencia reduces allowance with more people having to pay

the Impuesto Sobre el Patrimonio

Further to my article from last week, and after consultation with our accountant associates, it appears that the main residence wealth tax allowance of up to €300,000 only applies after 3 years of living in the property (habitual residence). This has been questioned but, as is often the case in Spain, getting a response from the tax office can be tricky.

The tax office words that are relevant in terms of getting around this 3-year rule are “circumstances that necessarily require the change of housing”. Moving to Spain to retire or for a change of lifestyle would not generally tick that box. If there are justifiable health reasons or similar then that appears to be acceptable in terms of applying the allowance.

To emphasise the habitual residence aspect, from JC & A Abogados in Marbella: “Please note that you must live effectively and consecutively in the property for more than 3 years, so you cannot rent the house out even for one day. In addition, you have to impute a benefit in kind for the Spanish property during the same 3 years period.”

In the words of JC & A, “The 3 year period starts counting from the purchase date as long as the dwelling is inhabited effectively and permanently within 12 months as from the purchase date.”

“…..a taxpayer who bought his main home but could not live in it because it was not suitable and had to have some works that exceeded 12 months; the conclusion is that the 3-year period starts counting from the date he moved in and not the purchase date.”

Adding salt to this potential tax wound, whilst it is not treated as your main residence (even though you live there permanently), you have to pay tax on its value as if you were a non-resident.

This all seems rather inequitable but is the law as things stand.

If you would like to discuss managing your money in these volatile and uncertain times, please do not hesitate to contact.

Visit John Hayward of The Spectrum IFA Group or complete the form below.

The Spanish State Pension

By John Hayward

This article is published on: 21st November 2022

21.11.22

How many years must one work in Spain to claim a Spanish State Pension?

When Brexit finally happened, one of the concerns that I had was regarding the bilateral agreement between the UK and Spain. I wanted clarification on whether years worked in the UK would continue to count towards the years required to qualify for the Spanish State Pension. The minimum number of years in the UK is 10 years but in Spain it is 15 years. Under the Trade and Cooperation Agreement made between the EU and the UK on 24th December 2020, and specifically the Article SSC.7: Aggregation of periods, it states that the periods of employment must be considered “as though they were periods completed under the legislation which it applies”.

How does this work in practice?

If someone has worked for 9 years in the UK and 14 years in Spain then, under the individual countries’ rules, neither minimum has been achieved. However, both countries’ rules are satisfied when adding the 9 to the 14 and vice versa. That is not to say that one would receive 23 years’ pension from either or both countries but merely that the person qualifies for a pension in both countries; 9 years’ pension in the UK and 14 in Spain. Details of how the pension is calculated can be found in my colleague Chris Burke’s article Claiming your UK State Pension whilst living in Spain/EEA.

Can you continue working in Spain whilst claiming a Spanish State Pension?

In the UK, you can receive your State Pension and continue to work. You will then only pay Class 4 National Insurance contributions, those associated with profit, as no further pension benefit will be accumulated. In Spain, you cannot claim your full State Pension entitlement if you continue working, and you do not employ anyone. However, it is possible to continue working beyond Spanish State Pension age and claim a reduced pension subject to certain conditions, one of these being that you must have achieved the minimum number of years to claim 100% of the Spanish State pension. This is currently 35 years but will be increasing over the next few years. You can once again apply the principle as discussed above in terms of adding the years in the UK to achieve this minimum.

To find out what your options are and how we can help you with your retirement planning, please contact me at john.hayward@spectrum-ifa.com or call/WhatsApp me on (0034) 618 204 731.